As part of the 2024 Budget, Chancellor Rachel Reeves has introduced a series of fiscal measures that could reshape the UK property landscape, particularly for landlords. Among these, the announcement of a rise in stamp duty for buy-to-let investors has captured significant attention. At Bricknells Rentals, we aim to keep our landlords and tenants informed about market changes that impact the rental property industry. Here, we outline what this shift could mean for landlords, the rental market, and what steps landlords can take in response.

What’s changing in stamp duty for buy-to-let properties?

Stamp duty has long been a point of contention in property investment, with buy-to-let properties currently subject to an additional 3% surcharge on top of the standard rates. Chancellor Reeves’ proposal builds on this surcharge with an extra increase specifically targeting investors. This aims to make property ownership more accessible for first-time buyers, while potentially discouraging buy-to-let investments that drive up demand (and, consequently, property prices).

For instance, an investment property valued at £300,000, which previously attracted a 3% stamp duty rate would now incur an additional 2%. This would make buy-to-let acquisitions notably more expensive. The increased costs could compel landlords to rethink their investment plans, as higher upfront costs reduce immediate returns and extend the time required to recover investments.

Potential impacts on the rental market

The move to increase stamp duty for buy-to-let properties will likely impact the rental market in several ways:

Reduced investment in rental properties: With increased acquisition costs, fewer landlords may choose to expand or maintain their portfolios, leading to a decrease in the supply of rental properties. In markets already experiencing a housing shortage, this reduction could exacerbate availability issues and limit rental options for tenants.

Potential rent increases: As landlords face increased financial burdens from the stamp duty rise, many will likely offset these costs by raising rents. With fewer available rental properties, demand-driven rent hikes could add further strain on tenants, particularly in high-demand urban areas.

Longer holding periods: Faced with higher upfront costs, landlords may opt to retain properties for longer periods, as flipping properties becomes less profitable. This could reduce property turnover rates, potentially limiting opportunities for new buyers, including first-time homeowners, to enter the market.

Alternative investments: Some landlords may consider diversifying away from residential property, choosing commercial real estate or other investment avenues that may be less impacted by increased stamp duty. This shift could also reduce the supply of quality rental housing.

How landlords can respond

Review investment strategies: With increased costs associated with new property acquisitions, landlords may need to rethink their approach to expansion. Diversifying portfolios, investing in property improvements, or consolidating existing assets could help maintain profitability.

Plan for the long-term: For landlords willing to take a long-term view, the reduced competition might ultimately lead to higher yields as demand outpaces supply. Holding properties for longer periods could also become a more viable strategy to balance initial stamp duty costs with rental income over time.

Pass on costs cautiously: While passing on some costs to tenants may seem like an immediate solution, landlords should be mindful of affordability concerns. Setting rent levels that are market-appropriate can help ensure tenant retention and long-term occupancy stability.

Seek professional advice: Navigating tax changes and understanding how they affect rental income and long-term investment strategy can be challenging. Seeking advice from property management experts, such as Bricknells Rentals, can help landlords make informed decisions in light of the new fiscal landscape.

Final thoughts

While the government’s aim to make homeownership more accessible is commendable, this stamp duty increase will undoubtedly introduce challenges for landlords, who play an essential role in housing the UK’s growing rental population. At Bricknells Rentals, we are here to help our landlords adapt to this changing environment and ensure they make the best decisions for their portfolios. Please contact us for advice on how to manage these and other legislative changes that affect your property investments.

For further information and assistance on navigating the evolving property landscape, visit Bricknells Rentals.

Recently, comments from Keir Starmer have reignited the discussion around the role of landlords in society, particularly around the notion that landlords may not be considered “working people.” This perspective can feel dismissive and overlooks the vital role landlords play in the UK economy, particularly in the property rental market. As a landlord-focused agency, Bricknells Rentals stands with landlords who are integral, hard-working contributors to our communities.

Landlords provide a critical service

Landlords offer housing options to millions across the UK, which is essential in a country where homeownership isn’t feasible or preferable for everyone. The range of rental properties they provide—from short-term rentals to long-term family homes—ensures there’s a diverse range of affordable and accessible housing options available. The rental sector plays a critical role in creating a stable housing market that can meet various financial and personal needs.

The investment is substantial and ongoing

Landlords work hard to acquire, manage, and maintain properties. They often invest substantial time, effort, and financial resources to maintain high standards for renters. Property investment isn’t a simple revenue stream; it involves responsibilities such as repairs, tenant management, staying informed on rental legislation, and ensuring the property is safe and comfortable. For many landlords, property management is their primary occupation—a full-time commitment that entails ongoing responsibilities.

Landlords drive economic activity

By investing in properties, landlords contribute significantly to the economy. Landlords create jobs, whether through employing tradespeople for maintenance, collaborating with property management agencies, or consulting with legal and financial advisors. This supports countless local businesses and trades, providing a consistent stream of work and income for others

Property investment is a legitimate income source

For many, becoming a landlord is a legitimate career choice. Whether they’re retired individuals supplementing their pensions, families investing to support children’s futures, or people who have shifted to property investment as a primary source of income, landlords represent a broad range of hard-working individuals. They are working people who take risks, dedicate resources, and add value to communities by helping tenants secure safe and affordable homes.

Rising costs are also affecting landlords

In recent years, landlords have faced increasing financial pressures, from rising property taxes and compliance costs to challenges posed by inflation and the cost of living. Many landlords have experienced increasing utility costs, property repairs, and tax obligations. Additionally, the evolving regulatory environment often requires significant financial outlay to ensure compliance. These costs are absorbed by landlords to support and improve their tenants’ living standards, further demonstrating their role as working individuals invested in their communities.

Building trust and partnership with tenants

The majority of landlords are focused on providing quality living experiences for tenants. Good landlords work to build trust, keep communication open, and foster positive relationships with tenants, many of whom rely on them for long-term housing stability. Agencies like Bricknells Rentals play an essential role here, helping landlords and tenants navigate these relationships to ensure everyone’s needs are met fairly.

As a dedicated property management company,Bricknells Rentals believes that landlords deserve recognition and respect for their hard work and commitment. They are working people, contributing to both the local and national economy, and are a vital part of the UK’s housing sector. It’s essential to view landlords as partners who are integral to community growth, housing accessibility, and economic stability.

The rental property market is on the brink of a significant shift, one that will undoubtedly cause concern among landlords across the UK. The new Labour government has made clear its intention to raise the minimum energy performance standards for rental properties, a move that could have far-reaching implications for both landlords and tenants alike. The proposed change, which would see the minimum Energy Performance Certificate (EPC) rating for rental properties increase from E to C by 2030, has sparked a mix of anxiety and uncertainty within the property sector.

The new regulations are part of Labour’s broader commitment to combat climate change and enhance energy efficiency across the nation’s housing stock. Yet this step isn’t the first foray by a government into improving the energy efficiency of the U.K.’s private rental homes.

The Tory government first introduced EPC regulations for private rental properties in 2018 as part of a broader effort to improve the energy efficiency of the UK’s housing stock. Under these regulations, landlords were required to ensure that their properties met a minimum EPC rating of E before they could be legally rented out. To support this, certain exemptions were allowed, and a cost cap was introduced, limiting the amount landlords were required to spend on energy efficiency improvements to £3,500 per property.

This cap was intended to prevent undue financial strain on landlords, particularly those with older or lower-value properties, while still encouraging necessary upgrades. The £3,500 cap covered a range of potential improvements, including insulation, heating system upgrades, and draught-proofing, and was seen as a balanced approach that allowed landlords to comply with the new standards without facing prohibitive costs.

The Scale of the Challenge for Rotherham Landlords

While the intentions of the Labour government are commendable, the practicalities for landlords are anything but straightforward. Upgrading a property’s energy efficiency from an E rating to a C rating is not merely a matter of a few minor tweaks like it was from taking a property from a G to an E rating; it often requires substantial investment. The reality of bringing a property up to a C rating could be vastly more expensive, with some projections placing the cost as high as £30,000 per property for older properties.

These figures are not just arbitrary; they reflect the significant work required to meet the new standards. From installing new insulation, upgrading heating systems, replacing windows, to potentially more extensive renovations depending on the property’s age and construction, the financial burden is considerable. For many Rotherham landlords, particularly those with older properties or properties where the value of rental homes are lower, the costs may seem prohibitive.

The Impact on the Rotherham Rental Market

The implications of these changes are likely to be profound. Some Rotherham landlords may decide that the cost of upgrading is simply too high and choose to sell their Rotherham properties instead. This exodus from the rental market could exacerbate the current housing shortage for tenants, driving up rents and making it even more difficult for those tenants to find affordable rental homes (although paradoxically, making buy-to-let more profitable for those that remain).

There is also the risk that the increased financial burden on landlords will be passed onto tenants in the form of higher rents. While the goal of improving energy efficiency is to reduce overall living costs for tenants by lowering their energy bills, this benefit could be offset if landlords raise rents to recoup their investment. This could particularly impact properties where rental incomes are lower, and the cost of upgrades represents a significant proportion of the property’s value.

Does Age, Tenure and Type of Home Make a Difference on the EPC Rating?

The EPC scores associated with each energy efficiency band are:

Band A – 92 plus (most efficient)

Band B – 81 to 91

Band C – 69 to 80

Band D – 55 to 68

Band E – 39 to 54

Band F – 21 to 38

Band G – 1 to 20 (least efficient)

Looking at only the property type, it certainly affects energy efficiency.

Overall, “flats and maisonettes” are the most energy-efficient property type in the UK, with a median energy efficiency score of 73, which is equivalent to band C. Detached and terraced dwellings came in second at 66 while in last place was semi-detached (65).

Detached homes tend to be more modern, so should have a higher energy rating. There are three external walls exposed in semi-detached houses, which would make you think it would have better EPC ratings than a detached. However, the average age of UK semi-detached homes is older than the average age of UK detached homes. Finally, the terraced home normally only has two external walls, so should be better than semis and detached homes. Yet, terraced homes have solid walls, which make them perform not as well as cavity walls. Finally, flats and maisonettes, which are more likely to be more modern and grouped in blocks, making them more efficient.

Energy Efficiency Across the Different Property Types and Their Tenure

Breaking down each type into its three tenures of owner occupiers, private renting and social renting…

Detached properties exhibit relatively similar energy efficiency ratings across all tenures, with owner-occupied homes scoring an average of 64, slightly higher than the private rented sector at 62, with social rented properties at 66. This suggests that while there is a marginal variation, social rented detached homes tend to be more energy efficient on average.

Semi-detached homes show uniformity in energy efficiency for owner-occupied and private rented properties, both with an average rating of 63. Social rented semi-detached homes, however, are somewhat more efficient, with an average rating of 68. This may reflect better insulation or energy-saving measures in the social housing sector.

Terraced properties reveal a small increase in energy efficiency as we move from owner-occupied (63) to private rented (64) and then to social rented (69). This trend indicates that terraced homes in the social rented sector might benefit from recent energy efficiency upgrades or more rigorous building standards.

Finally, flats and maisonettes demonstrate the highest energy efficiency ratings across all property types, with owner-occupied and social rented homes both scoring 72, and private rented properties closely following at 70. The higher ratings in this category could be due to the structural benefits of multi-unit buildings, such as shared walls that reduce heat loss.

In summary, while there are differences in energy efficiency across different property types and tenures, social rented properties generally exhibit higher energy efficiency ratings, particularly in the semi-detached and terraced categories. This may reflect concerted efforts within the social housing sector to improve energy efficiency, possibly driven by policy initiatives and funding targeted at reducing fuel poverty.

Energy Efficiency by Property Age

Finally, I just wanted to look at the age of the property and see if there is any difference.

The age of a home is also a key determinant of its energy efficiency, largely due to advancements in construction techniques and regulations over time. Properties built from 2012 onwards tend to have the highest energy efficiency, with a median score of 84, aligning with EPC band B. Homes constructed between 1983 and 2011 also perform relatively well, with a median score of 72.

Older properties, particularly those built between 1930 and 1982, have a lower median energy efficiency score of 65. The least energy-efficient homes are those built before 1930, which have a median score of 59, placing them in band E.

The concentration of older properties in an area can significantly impact its overall energy efficiency ratings, with areas of Rotherham containing a higher proportion of pre-1930 homes typically showing lower median scores.

The Regional and Local Rotherham Picture

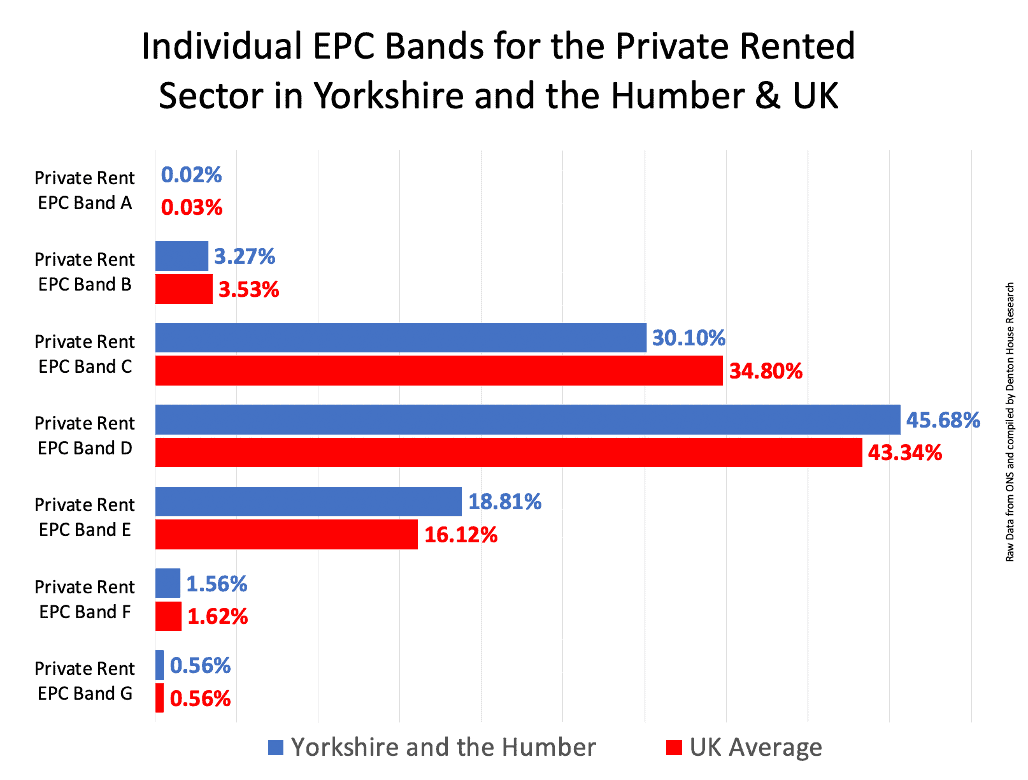

38.36% of UK private rented homes are in the proposed minimum EPC standards of A to C (compared to 33.39% in Yorkshire and the Humber). Nationally, 59.46% of private rented homes are in the D & E EPC ratings at the moment, (compared to 64.49% in Yorkshire and the Humber).

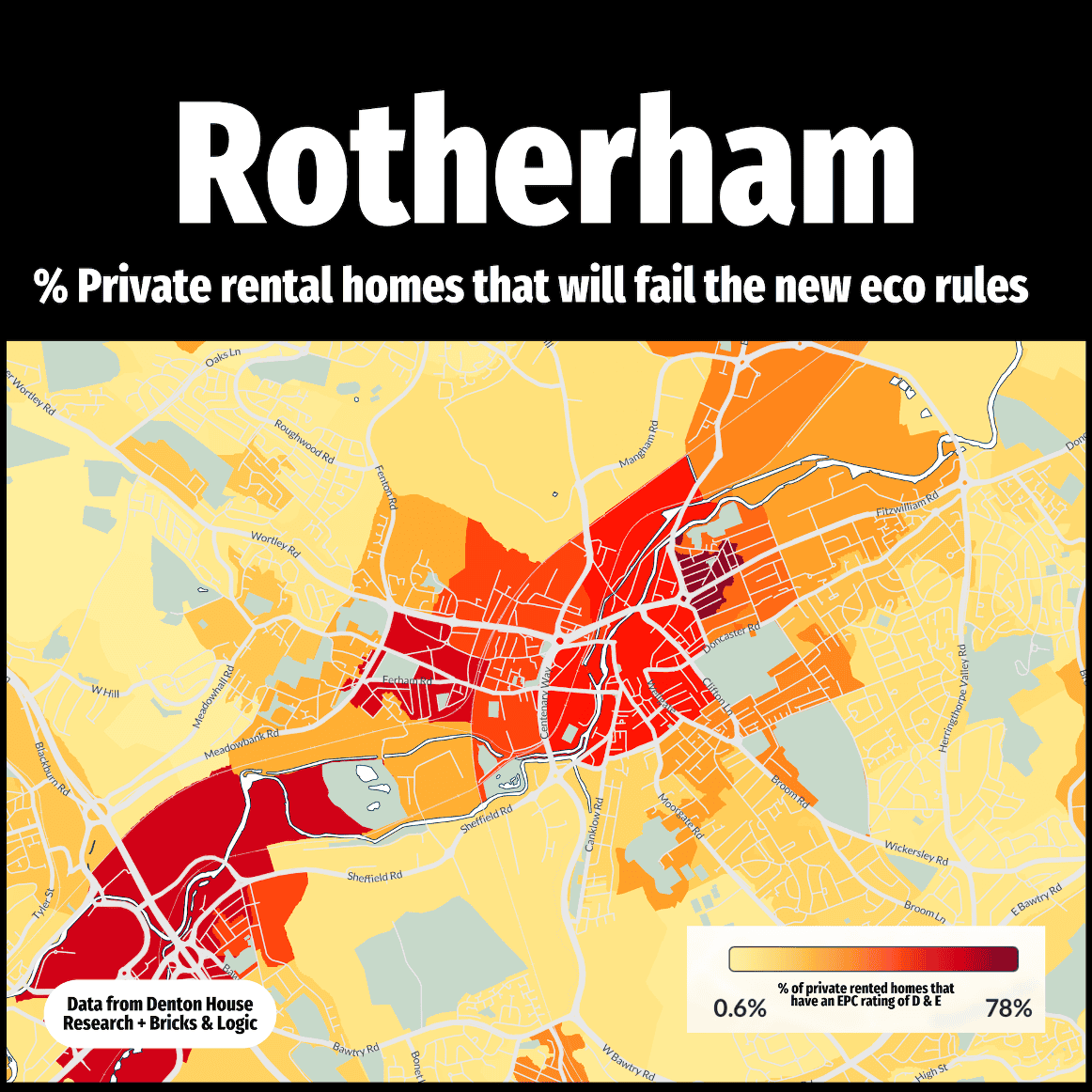

There are 5,376 private rented properties in Rotherham, of which 3,467 properties are in EPC Bands D and E.

To visualise that better, I have created this heat map to show the extent of the issue for Rotherham landlords.

Rotherham Landlords Navigating the Uncertainty

In the face of these challenges, it is crucial for Rotherham landlords to adopt a pragmatic approach. While the initial reaction may be one of concern, it is important to consider the long-term benefits of making these energy efficiency improvements. Properties with higher EPC ratings are not only more attractive to tenants, who are increasingly looking for homes with lower running costs, but they also tend to have higher market values. By investing in upgrades now, landlords can not only comply with future regulations but also enhance the value of their investments.

Moreover, there may be opportunities to mitigate the costs. The government has yet to finalise the details of the new regulations, and there is hope that they will introduce measures to support landlords through this transition. For example, there has been discussion around increasing the cap on allowable expenditure for energy efficiency improvements, potentially up to £10,000. Additionally, there may be grants, loans, or tax incentives available to help offset some of the costs.

Rotherham landlords should also consider the timing of their investments. While the 2030 deadline may seem distant, the scale of the work required means that starting early could be beneficial. Properties that are upgraded sooner rather than later will be in a better position to attract and retain tenants, particularly as energy efficiency becomes an increasingly important consideration for renters. Furthermore, by acting now, landlords can avoid the rush and potential price increases that are likely to occur as the deadline approaches.

It is also worth considering the broader societal benefits of these changes. Improving the energy efficiency of rental properties is not just about meeting government regulations; it is about contributing to the fight against climate change and helping to reduce the country’s overall carbon footprint. This is something that both Rotherham landlords and tenants can take pride in, and it aligns with the growing demand for more sustainable living options.

Moreover, the improvements made to properties will not only benefit current Rotherham tenants but also increase the long-term viability of the rental market. As properties become more energy-efficient, they will be better equipped to withstand future changes in energy prices and regulations. This future-proofs investments and ensures that landlords can continue to offer quality housing in a competitive market.

Final Thoughts: A Strategic Approach for Rotherham Landlords

In conclusion, while the proposed changes to EPC requirements may initially seem daunting, they should be viewed as an opportunity rather than a threat. By taking a proactive and strategic approach, Rotherham landlords can not only meet the new standards but also enhance the value and appeal of their properties. This will not only benefit their own portfolios but also contribute to a more sustainable and resilient local rental market.

The key is to start planning now, seek out advice from agents like ourselves or many of the other agents in Rotherham, and consider the long-term benefits of these changes. The road ahead may be challenging, but with careful planning and a commitment to improving the quality of rental housing, Rotherham landlords can navigate this transition successfully. As leaders in the property market, feel free to contact us to discuss what has been said in the article as it is everyone’s responsibility to not only meet these new standards but to embrace the positive changes they bring.

Membership of a Government-approved Client Money Protection (CMP) scheme became a legal requirement at the beginning of April 2019 for all agents in England dealing with residential lettings.

What does this regulation mean for landlords and how can you check that the letting agents that you work with comply with these regulations?

What is CMP?

CMP is a compensation scheme which recompenses landlords and tenants should an agent misappropriate their rent, deposit or other client funds.

From 1st April 2019, all letting agents in England risk facing fines for operating illegally if they have not joined an approved CMP scheme.

To be eligible for CMP, the legislation stipulates that agents must hold clients’ money in a separate bank account to operating funds and have the appropriate indemnity insurance so client money can be reclaimed if any employees commit fraud.

One positive aspect of a CMP is that it does not act on behalf of the letting agency. It is independent, providing protection of client money whilst being held by members and the scheme insures its liability for the payment of any claims.

What happens if my letting agency has not signed up to a CMP scheme?

If you are a landlord, it is essential that you check that your letting agency has a CMP scheme. If they have not, they are now breaking the law. More importantly for you, your money is not protected if that agent should misappropriate rent or other funds.

When you book a holiday, you don’t hand over your money to a travel agent if you don’t know your money is safe. The same now goes for property agents.

If your letting agents were to stop trading, your money would not be safeguarded, and you risk losing any rents or deposits held by the agent.

Before the legislation, it was estimated that only 60-80% of agents had voluntarily joined a CMP scheme. Not all agents were offering the security and reassurance to their clients that their money was safe. There will be rogue agencies that try to avoid their legal responsibilities – it is more important than ever to ensure your letting agents are members of a CMP scheme.

It is important that you can completely trust the agency who manages your properties. Thankfully, as you can see below, Bricknells Rentals are fully compliant with CMP regulations.

Bricknells Rentals: fully compliant with CMP regulations

You may have noticed the ARLA logo at the bottom of our website which is a sign that we are an ARLA Propertymark member. ARLA were actually instrumental in lobbying the government to raise standards in the lettings industry and make CMP a legal requirement. They led the campaign with support from our industry.

We are proud to be ARLA Propertymark members and pleased that it is a membership requirement to have CMP. We are members of their Government-authorised CMP scheme, which means that Bricknells are fully compliant with this regulation.

Agents must display a certificate confirming membership of an approved scheme in their branch and on their website. You can view our certification here.

As a landlord, what do I need to do?

The new law ensures that it is compulsory for agents handling money to have CMP but rogue letting agents are still in operation. Before handing money over or signing up to an agreement with a property agent, please make sure you see a copy of their CMP certificate. You can find a list of the schemes authorised by the government here.

An agent has misappropriated my money, what should I do?

It is clearly very important to check that your letting agent is not breaking the law and is fulfilling legal requirements by being a member of a Government-approved CMP. However, if you are unfortunately in a position where your rent or other money has been misappropriated, we recommend following these steps:

Report the misappropriation to the police.

Check that your agent is a member of CMP.

Contact the CMP and start the claims process – to do this you will need the tenancy agreement, the terms of business with the agent, bank statements illustrating a pattern of payments and then the non-payment by the agent and the tenant’s bank statements illustrating that rental payments have been made.

If the CMP finds that their member has misappropriated funds, then they will reimburse any client money found to be owing to you within the terms and conditions of their scheme.

If you do have any worries about the security of your rental income with other agents, then please get in touch with us. You can speak to our expert Chris Holmes by calling us: 01709 365 584

Bricknells Rentals is a letting agency that you can have complete confidence in.

To find a bargain you need to know the market, yet for all the talk about the property market in the UK, there isn’t really one property market. In fact, the British property market is like a fly’s eye – it looks one whole but in fact it is split into lots of fragmented pieces. What is happening here in Rotherham obviously is going to be different to other areas in the UK. Even in Rotherham, our property market is split into different patches due to school catchment boundaries or differing postcodes.

So what is going on in Rotherham?

We have noticed that the top end of the market (above £500,000) and the surrounding areas are proving a little tougher to shift than a few years ago. However, this can’t all be blamed on Brexit, as buyers have long been flinching at overestimated asking prices and excessive stamp duty rates.

Overall in Rotherham, 27.7% of properties for sale have reduced their asking price in the last 3 months by an average of 6.2%.

This is a lot less than the reductions that are being seen in central London. In fact, the property market in Rotherham is looking reasonably good with 41.8% of properties on the market in Rotherham being shown as under offer and sold subject to contract.

Are there any bargains in Rotherham? And if so, how do you find one?

To find a bargain you must know the local property market.

Start by comparing and contrasting properties, using sites such as Zoopla and Rightmove to see what’s for sale. The art here is to click on the ‘include Sold stc’ in the filters and then arrange them in price order. You will begin to get a feel for what properties are roughly selling for. You can also view recent sales (in Rightmove click on ‘House Prices’ on the main menu and then ‘Find Sold House prices’ on the drop down menu – you can even type in a street or street plus 0.25/0/5miles). There is a similar function in Zoopla (feel free to contact us if you need a hand with that).

Once you have found what you think is a bargain make sure you view it. Ask the agent why the sellers are moving. By doing your research on the seller, finding out how long it has been on the market, whether they have reduced the asking price (if you ask an agent they have to tell you and by how much) — you could cut a better deal if they are compelled to sell. It’s also vital to ensure that you are aware of the rental yields for that area – you can always get in touch for the expert advice if you are not sure how to estimate this. Push home your advantage (i.e. you don’t have a property to sell or you are a cash purchaser). This can make all the difference.

Expectations are probably at the lowest they’ve been for a good 10 years so landlords that use their heads are going to be able to take advantage of this ‘doom and gloom’ atmosphere that the media are creating. If you can find owners who are in the ‘got to sell’ category (instead of the ‘would like to sell’ category) then you may be able to find a dream property to purchase for your portfolio.

Like anything in life… buying a property bargain comes down to putting the hard-work in, doing your homework and jumping at opportunities. We do of course like to help landlords out – please visit out very helpful featured investment property deals page where we list bargains that we see on the market to get you started.

There’s been another delay to Brexit and more uncertainty for the UK – at least this time politicians have until 31st October to sort out this tricky mess! With Brexit in mind we wanted to look at the Rotherham property market. Is Brexit having a negative effect or are things continuing as before? It’s important for landlords to have this picture in mind as we continue to navigate through this potentially uncertain political and economic time.

How did Brexit impact the property market in 2018?

At the end of last year, we suggested property values in Rotherham would be between 1.3% and 2.3% different by the end of the year. It might surprise some people that Brexit hasn’t had the impact on the Rotherham property market that most feared at the start of 2018.

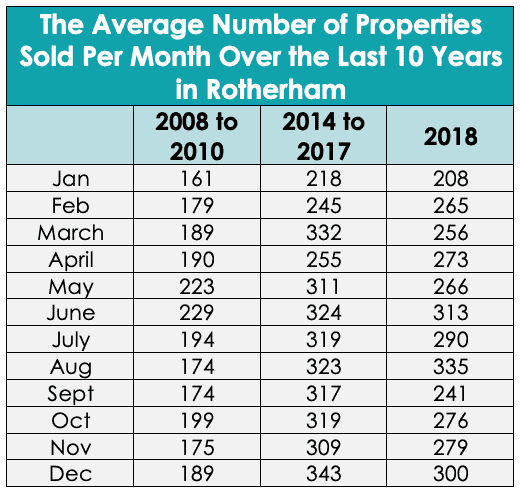

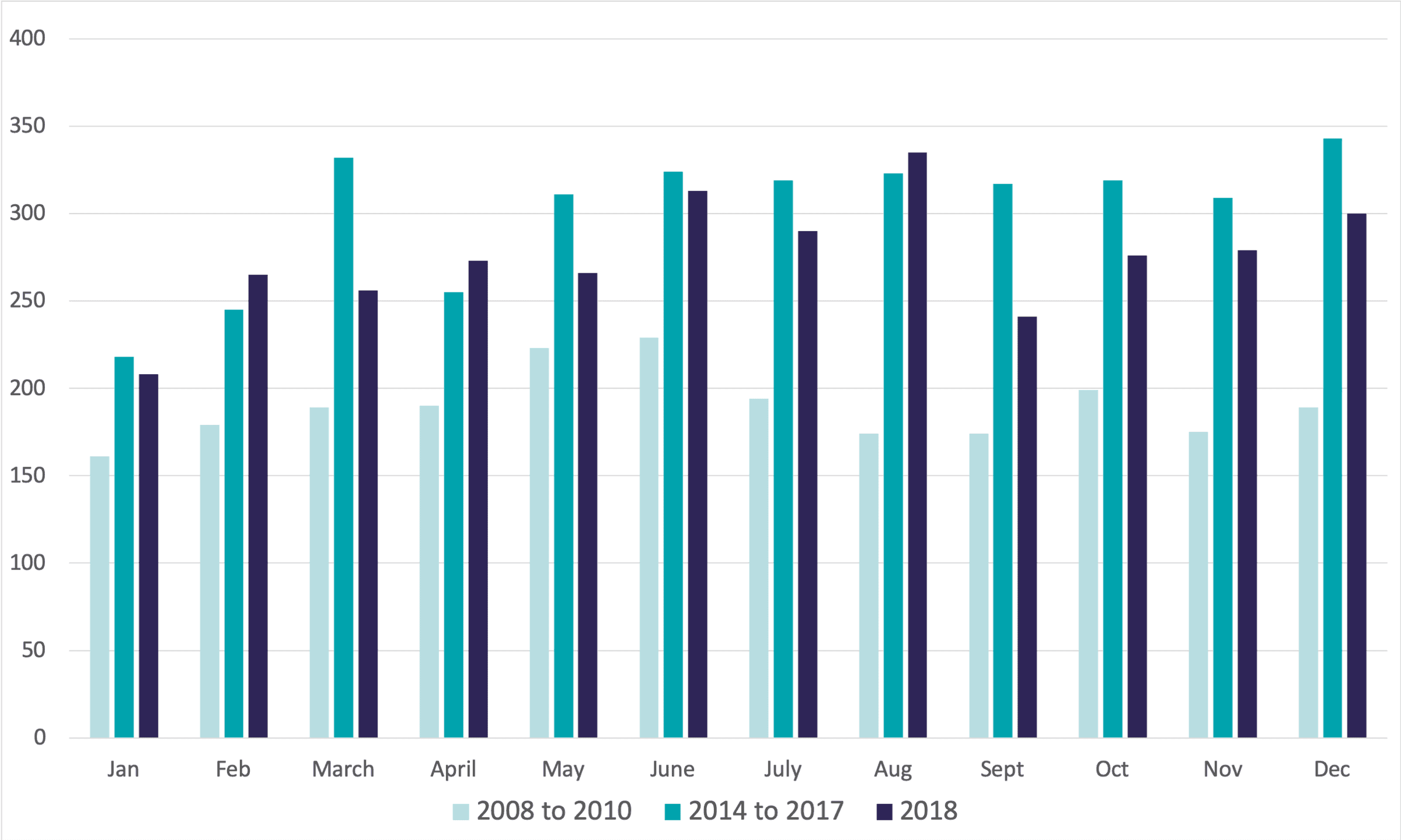

The basis of this point of view can clearly be seen in the number of property transactions (i.e. the number of property sold) that have taken place locally since 2008. The most recent property recession was the Credit Crunch between 2008-2010.

We decided to look at the 2018 statistics, and compare them with the Credit Crunch years (2008 to 2010) and the boom years (2014 to 2017). The results can be seen in this table:

From here we looked at the average quarterly figures for those chosen date ranges and created this chart:

In that 2008 to 2010 property recession, the average number of properties sold in the our area were 190 per month. Interesting when we compare that to the boom years of 2014 to 2017, when an average of 301 properties changed hands monthly. Last year, an impressive average of 275 properties changed hands monthly, still 45.1% higher than the Credit Crunch years of 2008 to 2010, despite the small drop compared to previous years.

Brexit is an unwelcome distraction from the real issues

The simple fact is the fundamental problems of the Rotherham property market are that there haven’t been enough new homes being built since the 1980s. Furthermore, the cost of buying your first home remains relatively high compared to wages and there have been tougher mortgage rules since 2014.

It is these issues which will ultimately determine and form the rather unexciting, yet still vital, long term outlook for the Rotherham (and national) housing market. The Brexit issue is just a diversion away from the real issues that we need to worry about. Assuming something can be sorted with Brexit (eventually!), in the long term property values in Rotherham will be constrained by earnings increases with long term house price rises of no more than 2.5% to 4% a year.

Landlords: “Should I wait to buy or not?”

This is the question landlords keep asking us. Do we wait for Brexit to get sorted or do we buy now?

Well, our answer is often a question: where else are you going to invest your money? We have already mentioned that we aren’t building enough homes to keep up with demand… so as demand outstrips supply, house values will continue to grow. Putting the money in the building society will only get you 1% to 2% if you are lucky. Property remains an excellent investment.

Furthermore, in the short term, there could be some bargains to be had from shortsighted panicking sellers. There are often great opportunities to be had and this is why we keep posting property recommendations here.

What might be happening is that normal homebuyers are putting off moving due to Brexit. Therefore, when the Brexit issues are finally sorted out in October (or sooner!) we may see a release of that pent-up demand to move home, increasing the price for buy-to-let landlords and investors.

The proportion of 25 to 34-year olds who own their home in Rotherham has dropped by more than a third in the last 20 years. What does this mean for all the existing Rotherham landlords and homeowners (as well as all those youngsters dreaming of one day buying their first home)?

Let’s start by taking a look at the numbers in greater detail. In Rotherham there has been a 36.0% proportional drop in the number of 25 to 34-year olds owning their own home between 1999 and 2019. During the same time frame there has been a smaller drop of 18.1% of 35 to 44-year olds owning their own home.

Therefore, if you were born in the late 1980s or early 1990s, the dream of owning a home in Rotherham has reduced dramatically over the past 20 years.

Are there any particular reasons?

The most prominent reason is that young adults’ salaries are now much lower in relation to Rotherham house prices. Nationally, average property values have grown by 186.9%, whilst average incomes have only risen by 44.8%, yet that doesn’t allow for inflation. However, whilst not over the same 20 years (it’s close enough though), the Institute of Fiscal Studies said recently the average British home was just over 2.5 times higher in 2015/6 than in 1995/6 after allowing for inflation – yet the average household income (after tax) of 25 to 34-year olds grew by only 22% in ‘real-terms’ over those 20 years.

Yet, even though property prices are at record highs, on the other side of the coin, the monthly cost of mortgage payments has actually fallen because interest rates have remained low. In 1999, the average mortgage rate paid by UK homeowners was 6.54% whilst today it’s more than halved to 2.64% – a drop of 59.4%. Many of you reading this will remember the 15% mortgage rates of 1992!

The fact is t mortgage repayments take up a considerably smaller proportion of take home pay, on average, than they did before the Credit Crunch or in the late 1980s. Although the risk that mortgage rates will increase if the Bank of England put up interest rates might leave some homeowners in a difficult position – hence I might suggest (if you haven’t already) you seriously consider fixing your mortgage rate (remember to take advice from a professional before you do).

Yet look at the data in even greater detail and you will see, going back to the 1960s, we weren’t always the huge homeowning nation we always thought we were.

Today, 18.4% more 35 to 44-year olds and 51.3% more 45 to 54-year olds own their own home compared to 1969, and if you look at the graph, move the clock back to the early 1960s and you will see the numbers are even starker. So as the younger generation in Rotherham has seen homeownership drop in the medium term, they will in fact end up inheriting the homes of their parents. We are turning into a more European (especially German) model of homeownership, where people buy their first home in their 50s instead of their 20s.

Our message to first time buyers in Rotherham

Our message to first time buyers of Rotherham is go and get some mortgage advice! The cost of renting smaller starter homes is between 20% and 25% more than the mortgage payments would be. 95% mortgages (meaning a 5% deposit is required) have been available since late 2009 and some banks even do 100% mortgages (i.e. no deposit). I suggest that you don’t assume you can’t get a mortgage – for the sake of a 45 minute chat with a mortgage adviser – you get a straight answer and all the information you need.

What does this mean for landlords in Rotherham?

Ultimately, this is great news for landlords. For many tenants, renting is a positive choice so if you keep your property fairly well maintained, there should always be demand for it to be let. Furthermore, as we aren’t building enough homes to meet the current demand, home values will (over the medium to long term) rise above inflation. Therefore, the property market, despite new legislation, is still a worthwhile and positive investment. Good news for Rotherham landlords and homeowners alike.

The single biggest issue in the country (and Rotherham) today is that we aren’t building enough homes. We know it seems the local area is covered with building sites – yet looking at the actual numbers – we still aren’t building enough homes to live in. Residential property only takes up 1.2% of all the land in the UK – and whilst we’re not suggesting we build housing estates on National Trust land or cut down forests, until we realise that we aren’t building enough… this issue will only continue to get worse.

Advice for landlords

If you are a landlord and need our expert advice, please get in touch. We’re always happy to help and provide valuable insights into the local market. We want to support you and help you make the most of your property portfolio.

If you watch the national news you will notice that, especially when it comes to talking about the property market, it is incredible London-centric. In facts over the last 5 years, the London property market has really manipulated the UK on averages to such an extent that many lenders like the Halifax and Nationwide now publish two indices, one with London included and one without.

It is true that the London property market has undergone some acute property price falls. In the upmarket areas of Mayfair and Kensington, the Land Registry have reported values are 11.3% lower than a year ago, yet in the UK as a whole they are 1.3% higher. If you look around the different areas and regions of the UK and Northern Ireland, property values are up 5.8% year on year. More specifically, Yorkshire is 3.7% up.

So, what exactly is happening in Rotherham?

Well, to start with, as we have been saying for a while now, property is a long game, and making decisions on the short-term fluctuations is something that could cause a nervous breakdown. Landlords need to really consider this.

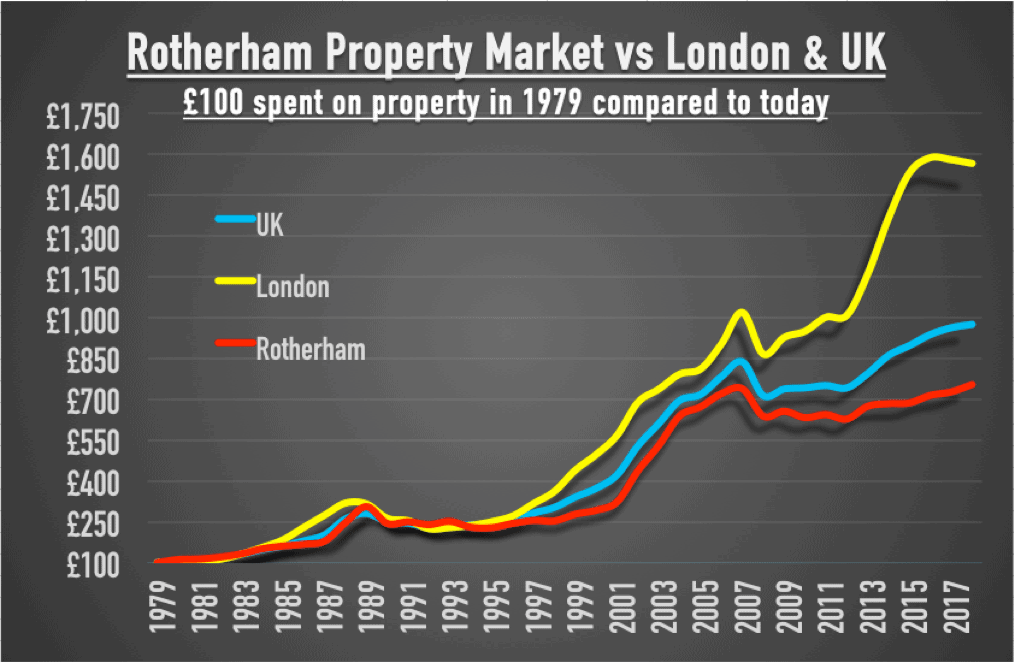

It’s interesting to compare Rotherham to London and the UK as a whole but this is quite hard to do as the average value of a property in Rotherham obviously differs significantly in comparison to the one in the capital. To compare like for like, we need to see what would happen if we had spent £100 on a property in London in 1979 and what that £100 would be worth today.

Therefore, let’s take a look at the last 40 years:

Can you see how the growth of that £100 was broadly similar between 1979 and 2007 on all three strands of the graph? After that the credit crunch caused a drop between late 2007 and 2009. After that time though, London has gone on a very different trajectory to the rest of the UK. Whilst Rotherham has continued to be generally subdued between 2009 and 2012, London pressed on. All areas of the country had a temporary blip in 2012 but, whilst Rotherham and the UK went up a gear again 2013, London went into overdrive and up like a rocket!

Are price falls likely to spread?

London has dipped slightly in the last year so the hot question for everyone has to be: are price falls likely to spread (as they did in the previous property recessions of 1989 and 2007) to Rotherham and other places in the UK? The Bank of England’s opinion is that a London house price drop is unlikely to be the beginning of a countrywide trend. Looking at the graph again, it can be seen London has been in decline for 2 years, whilst the rest of the country has been moving forward.

What does all this mean for Rotherham homeowners and landlords?

Well what happens in London does have an impact, but there are other issues that will have a bigger impact on the local property market. The simple fact is over the last 40 years, we have had 392.9% inflation. Looking at a typical Rotherham terraced house, it has jumped in value from an average of £9,089 to £97,800 since 1979 (a rise of 654.2%).

Property has, in the long term, been a good bet. Yes, we might have some short-term blips but as long as you play the long game – you will always win.

In the short term, our concern isn’t over monthly up or down property values, Brexit or another General Election. With property values still rising faster than salaries in many parts of the country, what really matters is how much of householder’s take home pay goes into housing costs as opposed to other spending items. If housing gets too expensive – other things will suffer, like holidays and the nice things in life to spend your money on. Only time will tell!

Whilst comparing Rotherham and London can be seen as a bit of fun, we are in the business of giving valuable advice to landlords – just take a look at our blog! If you are a landlord in need, please get in touch and we will do our best to provide you with our high quality advice.

We are delighted that our Managing Director, Dawn Holmes, has been invited to participate in a Parliamentary Review about the lettings industry. Read more in the recent coverage by The Rotherham Advertiser (click the image to enlarge).

The government are preparing to control tenant’s deposits, limiting them to five weeks rent. This will mean that landlords will soon only be protected in the event of a single month of unpaid rental arrears, at a time when Universal Credit introduction issues has seen some rent arrears quadrupling (and that’s before landlords consider damage to property and solicitor costs).

It’s important to consider both sides of the story: it can’t be disputed that the deposits tenants have to save for raises the cost of renting. It puts another nail in the coffin of the dream of home ownership for many Rotherham renters. At the same time, those same deposits are unable to provide landlords with a decent level of protection against unpaid rent or damage to the property.

What’s going on in Rotherham?

Let’s look at the facts in our area: in Rotherham there is a combined total of over £4,660,000 in deposited or protected tenant deposits.

However, when you consider the value of all the privately rented properties in our area totals £819,600,000, you can see the need for decent landlord insurance to ensure adequate cover for the Rotherham landlord.

Again, let’s consider the point of view of the Rotherham tenant. Several housing charities believe spending more than a third of someone’s salary on rent as exorbitant, yet for the tenants they find themselves in that very position. We feel especially sorry for the Rotherham youngsters in their 20s who want to rent a place for themselves – they face having to pay out the rent and try and save for a deposit for a home.

Here’s the reality for Rotherham young people…

The average 22 to 29-year-old in Rotherham spends 28% of their typical salary on a one bed rental property

….and 32% of their salary for a 2-bed home in Rotherham.

How does this compared to history?

40 years ago, British people who rented spent an average of 10% of their salary on rent, and only 14% in London. Looking in even greater detail, according to the ONS, over the past 60 years the proportion of total spending on all housing (renting and mortgages) has doubled from 9% in the late 1950’s to 18% today. Whilst, on the other hand, the proportion of total expenditure on food has halved (33% to 16%), as has the proportion of total spending on clothing (10% to 5%).

Landlords have important costs that need to be considered

Landlords also face costs that need to be covered from rents including mortgages, landlord insurance (especially the need for the often inadequate deposits to cover the loss of rent and damage), maintenance and licensing. In fact, rents in the last 10 years have failed to keep up with UK inflation, so in real terms, landlords are worse off when it comes to their rental returns (although they have gained on the increase in Rotherham property values – but that is only realised when a property sells).

There are a small handful of Rotherham landlords selling some/or all of their rental portfolio as their portfolios become less economically viable with the recent tax changes for buy-to-let landlords. We predict that this will result in fewer properties available to rent, reducing the supply and availability of rental properties in our area and inevitably causing rents to rise. For those landlords that keep their properties, they could actually end up seeing return and yields rising.

Yet, because tenants still can’t afford to save the deposit for a home and we are all living longer, the demand for rental properties across Rotherham will continue to grow in the next twenty to thirty years as we turn to more European ways where the norm is to rent rather than buy in the 20s and 30s age range. Things often go in full circle: this could mean new buy-to-let landlords will be attracted into the market.

It’s a complicated time and many landlords are getting in touch with us for our advice and support. We are always happy to help so please do get in touch. Our details are on the contact page. For those looking to invest in the property market, we post several property recommendations to our investment property deals page.

ompared to 1969, and if you look at the graph, move the clock back to the early 1960s and you will see the numbers are even starker. So as the younger generation in Rotherham has seen homeownership drop in the medium term, they will in fact end up inheriting the homes of their parents. We are turning into a more European (especially German) model of homeownership, where people buy their first home in their 50s instead of their 20s.

ompared to 1969, and if you look at the graph, move the clock back to the early 1960s and you will see the numbers are even starker. So as the younger generation in Rotherham has seen homeownership drop in the medium term, they will in fact end up inheriting the homes of their parents. We are turning into a more European (especially German) model of homeownership, where people buy their first home in their 50s instead of their 20s.